"I have two great enemies, the Southern Army in front of me, and the financial institutions in the rear. Of the two, the one in my rear is my greatest foe." -Abraham Lincoln

"You are a den of thieves and vipers, and I intend to rout you out, and by the Eternal God, I will rout you out." -President Andrew Jackson to the bankers in 1835

By 1836 Andrew Jackson had successfully killed the Second Bank of the United States and in only two years (by January 8, 1838) he paid off the entire national debt. When he was asked what his most important accomplishment had been, he stated without hesitation, "I killed the bank."

On June 4, 1963, President John F. Kennedy (executive order 11110) declared that the privately owned Federal Reserve Bank would soon be out of business.

Subscribe to:

Post Comments (Atom)

30 comments:

Here is how representatives from Illionis voted on the bailout:

Democrats: Bean, yes; Costello, no; Davis, yes; Emanuel, yes; Foster, yes; Gutierrez, yes; Hare, yes; Jackson, no; Lipinski, no; Rush, no; Schakowsky, yes.

Republicans: Biggert, no; Johnson, no; Kirk, yes; LaHood, yes; Manzullo, no; Roskam, no; Shimkus, no; Weller, not voting.

me don't understand! Banks are the major reason we're in a mess and the government makes it easier for them to get in trouble again; namely, the clause in "plan b" of the "Bailout":

when the market for mortgage related securities dries up, companies can value them based on their estimated future cash flow. Some experts blame the previous rules, known as mark-to-market, for the credit crisis.

Changing the accounting rule from "marked to market" to "marked to future market" sure provides me with more confidence in the banks.

OK...here's a plan I could live with.

I'm against the $85,000,000,000.00 bailout of AIG.Instead, I'm in favor of giving $85,000,000,000 to America in a We Deserve It Dividend.To make the math simple, let's assume there are 200,000,000 bonafide U.S. Citizens 18+. Our population is about 301,000,000 +/- counting every man, woman and child. So 200,000,000 might be a fair stab at adults 18 and up..

So divide 200 million adults 18+ into $85 billon that equals $425,000.00.My plan is to give $425,000 to every person 18+ as a We Deserve It Dividend. Of course, it would NOT be tax free.So let's assume a tax rate of 30%. Every individual 18+ has to pay $127,500.00 in taxes.

That sends $25,500,000,000 right back to Uncle Sam. But it means that every adult 18+ has $297,500.00 in their pocket. A husband and wife team has $595,000.00.What would you do with $297,500.00 to $595,000.00 in your family?

Pay off your mortgage - housing crisis solved.

Repay college loans - what a great boost to new grads

Put away money for college - it'll be there

Save in a bank - create money to loan to entrepreneurs.

Buy a new car - create jobs

Invest in the market - capital drives growth

Pay for your parent's medical insurance - health care improves

Enable Deadbeat Dads to come clean - or else

Remember this is for every adult US Citizen 18+ including the folks who lost their jobs at Lehman Brothers and every other company that is cutting back. And, of course, for those serving in our Armed Forces.

If we're going to re-distribute wealth let's really do it...instead of

trickling out a puny $1000.00 ('vote buy') economic incentive that is being proposed by one of our candidates for President.

If we're going to do an $85 billion bailout, let's bail out every adult U S Citizen 18+! as for AIG - liquidate it.Sell off its parts. Let American General go back to being American General. Sell off the real estate.Let the private sector bargain hunters cut it up and clean it up.Here's my rationale. We deserve it and AIG doesn't.

Sure it's a crazy idea that probably would'nt work.But can you imagine the Coast-To-Coast Block Party! How do you spell Economic Boom? I trust my fellow adult Americans to know how to use the $85 Billion We Deserve It Dividend more than do the geniuses at AIG or in Washington DC .And remember, This plan only really costs $59.5 Billion because $25.5 Billion is returned instantly in taxes to Uncle Sam.

This is a nice idea but the placement of the decimal isn't correct:85 billion divided by 200 million is $425 and not $425,000 unless you're doing "marked to future" pricing.

The sweetened bailout was signed by Bush today. The following lists how the Reps from Illinois voted (Weller voted yes on the "rescue"):

Democrats — Bean, Y; Costello, N; Davis, Y; Emanuel, Y; Foster, Y; Gutierrez, Y; Hare, Y; Jackson, Y; Lipinski, N; Rush, Y; Schakowsky, Y.

Republicans — Biggert, Y; Johnson, N; Kirk, Y; LaHood, Y; Manzullo, N; Roskam, N; Shimkus, N; Weller, Y.

Senators Durbin and Obama both voted yes for the bill.

Here is Rep. Paul on the biggest bailout in the government’s history, words he wrote before the U.S. House of Representatives voted to approve the bill:

This time last week, the biggest bailout in the history of the world seemed to be a fait accompli.

Last weekend, the Fed Chairman and the Secretary of the Treasury had harsh words of doom and gloom for Congressional leaders, with the rest of the administration parroting along, and by last Monday it seemed both parties were about to fall in line and vote our Republic away by socializing the banking industry through this bailout.

Foolish business behavior was about to be rewarded, and propped up a little longer, the bubble blown a little bigger, and our coming Depression made that much greater, but then something happened on the way to the House floor.

Citizens made their voices heard.

The real story behind the story in Congress this week was the thousands of calls and emails sent to Representatives, clogging up inboxes and even slowing down the House internet system.

Slowly, like the Titanic turning around, sentiments on the Hill shifted, and we heard Congressmen capitulating and changing their tune a little, desperately trying to find ways to salvage the bailout without completely enraging their constituencies.

Now we hear about taxpayer protections, about golden parachutes, and about other nuances that hardly cover up the fact that we would be creating more money out of thin air and further devaluing the dollar!

The problem is not HOW the government is spending this money; it’s the fact that the government is spending this money. We don’t have it. We are already nearly $10 tn in debt, not including unfunded liabilities.

We already spend about $1 tn a year we don’t have on our overseas empire. Now nearly $1 tn more is somehow supposed to magically appear and solve all our problems! No — creating more money might delay the inevitable for some well-connected banks on Wall Street, but in a few weeks we will find ourselves right back in this same position, but much poorer.

The unfortunate thing is that we’ve already spent at least $700 bn on other bailouts that did not solve the problem. And while all this negotiation was taking place, the auto industry was quietly bailed out, with no controversy, no discussion, to the tune of $25 bn.

Inevitably, it appears Congress will call their constituents’ bluff and the bailout will pass, because that is the habit Wall Street and Washington have fallen into. People are right to be concerned about our financial future.

I’ve been talking for 30-some years about reasons we need to be concerned and change our ways. We find ourselves now in a position of no good options, and no silver bullets.

But the worst thing we can do is to compound our problems by intensifying the mistakes of the past.

We do have tough economic times ahead, no doubt, no matter what we do, even if we do nothing.

The question is, will we have the courage to take our medicine now and get it over with, or will we prolong the misery for many years to come? I’m less and less optimistic about the answer to that question.

Less than two weeks after Uncle Sam gave American International Group (AIG) an $85 billion loan - staving off financial collapse - execs from one of its insurance subsidiaries, AIG American General, gathered for a conference at the uber-s**** St. Regis Monarch Beach Resort, billed as “California’s only Mobil Travel Guide Five-Star Resort,” where ocean-view rooms start at $565 a night and “world class luxury” is the rule.

On Friday, before the presidential debate got under way, caterers for the St. Regis were setting up dozens of tables on the grounds of Mission San Juan Capistrano for AIG American General’s sumptuous off-site dinner. Tables were draped with soft Tuscan-gold tablecloths that cascaded to the grass; elegant fresh flower centerpiece graced each table; and what appeared to be fine crystal stemware, at least from a distance, glistened in the fading light.

Workers set up a lengthy bar stocked with bottles of liquor. A half-dozen tall space heaters stood sentinel in case the evening turned cool. There was a large center stage with lighting and a sound system, and once the sun went down, the whole scene took on a magical patina as tiny white lights twinkled in the trees.

The Watchdog - and the Outraged Taxpayer who alerted us to the situation - understand that corporate events such as these are planned many months in advance. I mean, really. Who could have known in the spring that there’d be Financial Armageddon in the fall?

But still. “The inappropriateness and the excessiveness just blew us away,” said the Outraged Taxpayer, who went to the Mission Friday to pray in the chapel. “It’s outrageous. In very poor taste. Over the top.”

http://waronyou.com/2008/10/aig-subsidiary...-after-bailout/

Iceland Bankrupt?!

Banks are nationalized and make sweeping new powers that allow the government to take over companies, limit the authority of boards, and call shareholder meetings.

http://news.yahoo.com/

s/ap/20081007/ap_on_re_eu/eu_iceland_meltdown

The construction of the “house of cards” was created in steps by the erosion of the Glass-Steagall Act of 1933. The Glass-Stegall Act entailed many provisions to regulate the banking industry’s way of doing business. The Glass-Steagall Act prohibited a bank from offering investment, commercial banking, and insurance services. The deregulation of banks through numerous repeals of the Glass-Stegall Act is what created the speculation in this house of cards. Through the Depository Institutions Deregulation and Monetary Control Act of 1980, which allowed banks to merge, coupled with the Gramm-Leach-Bliley Financial Services Modernization Act of 1999, which permitted competition among banks, securities companies and insurance companies, are, IMO, the major causes for today’s woes in the financial industry…very similar to pre-1933.

Our political representatives have again failed to learn from history and bit on satisfying the never-ending greed of their contributors/lobbyists. Would reform on lobbying and political contributions help stop this from happening again?

Dear Anonymous, October 12:

You ask " Would reform on lobbying and political contributions help stop this from happening again?"

Only if "We the People" wake up...

Reform must take place by DEMANDS FROM the American People.

If wealthy, powerful organizations/groups wish to lobby --- they need to lobby TO THE PEOPLE- not to the government. Then ask for the people speak to the government.

Political contributions should ONLY be allowed by individual people.. not, from again, the pockets of the wealthy, powerful organizations/groups.

WHICH include the political parties...republican/democratic parties. (a loaded statement I'm sure)

"We the People" has turned into "We the organizations/the groups with the MOST MONEY" - and not let us forget - "THE MEDIA".

And "We the People" let it happen.

Anyone out there have a tea bag they would like to donate?

The economy and tax plans are vital issues. How do the candidates stack up?

McCain wants an additional $170 billion a year in tax breaks for large corporations with $3.8 billion going to the 5 largest oil companies every year.

Obama wants to cut taxes for about 98% of American families and will only raise taxes for those making above approximately $600,000 per year.

Obama will specifically raise taxes on corporations who are outsourcing large numbers of jobs.

McCain? In a nutshell, the Oil Companies McCain is giving so much to are history. Supporting Oil companies in a time when we should be switching from fossil fuels is backwards.

The most important part of the American economy is the middle, poorer, and upper-middle classes. This is the vast majority of people. If raising taxes on the extremely wealthy brings in more taxes then raising them on everybody, then that plan will better the economy.

Obama will raise taxes on outsourcing companies, making it more profitable to give more jobs to Americans. This can only help the economy.

Obama wants to lower taxes for 98% of Americans, give more jobs to Americans instead of over seas, support American-based jobs and advances in alternative energies, which will get the economy flowing again, and most importantly:

End the war.

By the way, the war is the SINGLE biggest deductor from our economy.

As of right now, approximately $589,788,089,532 has been spent towards the war.

This money could have been spent repairing and upgrading all schools in our country. What this money could have done is huge and would have positively changed America for generations. McCain wants to add, add, and add to it. His motto has been "More to the War, less to America".

A war with Iran would be a complete disaster.

What was the song McCain sang? "Bomb, Bomb, Bomb; Bomb, Bomb Iran?"

The tag team of JPMorgan as the monster and Goldman Sachs as its harlot represent a powerful pair that is more responsible for destroying the entire US financial system than 95% of the American public has any awareness. The colossus of JPMorgan is a monster, a predator, nurtured by pond scum. It has gobbled up Chase Manhattan, Manufacturers Hanover, Chemical Bank, Bank One, and more over the past two decades. Their profound presence in keeping the USTreasury Bond yields down can never be understated. They do so by managing 85% of the credit derivatives on the planet.

Wall Street Monsters & Meat (You)

http://www.financialsense.com/fsu/editorials/willie/2008/1016.html

Heard on the street (or should I say alley): Be very leary of gold certificates...some believe many of these certificates have no intrinsic value because the amount of gold represented by the certificates far outweighs the amount of gold that actually exists.

One analyst believes that the market has been dumped with a bunch of gold certificates to artificially keep the price of gold down to mislead the public that the economy isn't that bad.

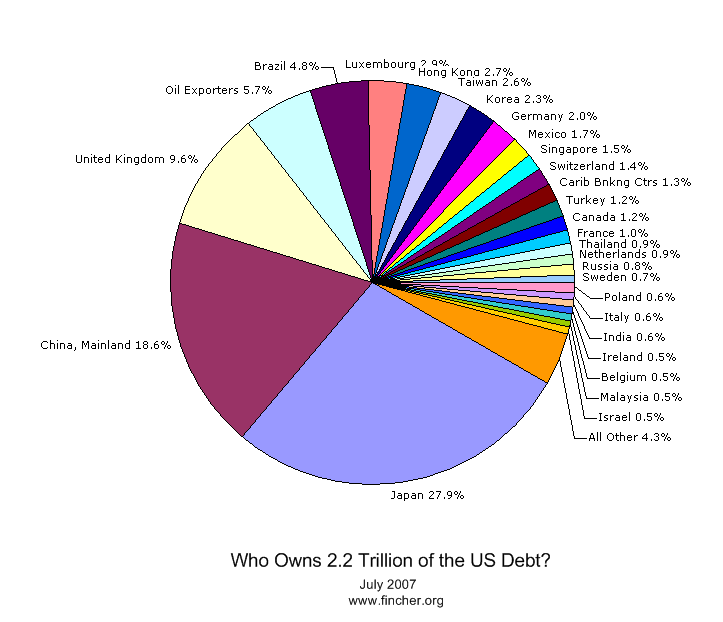

We're now $10 trillion in debt

(that is $10,000,000,000,000).

That is over $33,000 per person (men, women, and children) in the United States.

Nearly half of this has gone to bailing out mismanaged companies.

Thanks George Bush, Dick Cheney, Dick Durbin, Barack Obama, and Jerry Weller. Thanks for being negligent in your duties.

to tj,

In light of your post, I've posted a line graph (with hyperlink) of the National Debt since 1938 to the present on the main page. It is sad to see the rate of increase in the past 20 years.

End of Fiscal Year

US Gross Debt as % of GDP[20]

(http://en.wikipedia.org/wiki/United_States_public_debt

1940 52.4%

1950 94.1

1960 56.1

1970 37.6

1980 33.3

1990 55.9

2000 58

2005 64.6

2007 65.5

2008 72.5 (EST)

Intersting read of the history of the U.S. National Debt: http://www.cedarcomm.com/~stevelm1/usdebt.htm

to verity quest,

Good information.

I would be interested in seeing the amount(s) of American citizen debt since 1938.

Also the dollars donated to charity, churches, etc by American citizens annually since 1938.

Thanks.

To 8:02am,

Here is some info on consumer debt from the Fed:

http://www.federalreserve.gov/

releases/g19/current/default.htm

Here is another site, not sure of its validity though:

http://mwhodges.home.att.net/

nat-debt/debt-nat.htm

Their has been massive purges of voters in the primaries. Be sure to check your registration and polling place. Don't take a chance on losing your vote in November.

Make sure you are registered to vote by the deadline in your state, and find out where you vote on election day. Many voters went to the polls in the primary election and discovered they weren't on the registration rolls. Don't let that happen to you.

Call your local election office (Grundy County Clerk's phone number is 815-941-3222) today to make sure your vote counts. Spread the word.

Trickle doesn't work!

Oct. 20 (Bloomberg) -- Nripata Ray, manager of Wall Street Caterers in New York's financial district, says business hasn't been this bad since the 2001 terrorist attacks.

``We are watching what's going to happen next and we can do nothing,'' said Ray, whose customers included Lehman Brothers Holdings Inc., now bankrupt, and American International Group Inc., which had to be bailed out by the government. He may have to get rid of some of his 16 employees, Ray says.

The collateral damage from the worst financial crisis since the Great Depression is spreading in New York, slashing business from caterers to limo services to stationers.

``For those that had a strong share of their business coming from Wall Street, they're going to be vulnerable to the contraction,'' said Doug Turetsky, a spokesman for New York's Independent Budget Office, a city government fiscal monitor.

The city may lose as many as 165,000 jobs in the private sector over two years, including 35,000 in the financial industry, Comptroller William Thompson said last week. The projected job losses were 80,000 more than Thompson's last budget report in July.

The securities industry accounts for 5 percent of jobs in the city and 23 percent of all compensation.

Resumes Soar, Offers Plunge

Headhunter John Warren, president of New York's A-List Associates Inc., said the number of resumes he gets daily has tripled to 150, and job offers have dropped 60 percent. About 90 percent of his customers are from Wall Street, he said.

``It's a lot tougher,'' Warren said. ``People take anything right now.''

Club Quarters, a New York membership hotel on William Street in the financial district, had 20 to 30 rooms available in the past few weeks, compared with the usual four it has around this time of year, said Anisul Islam, a guest services manager.

``Some of our guests specifically called and said `I'm not going to come because I lost my job,''' he said.

LimoRes.net, a Web site that books car services through a network of 7,000 limousine services worldwide, has seen a 50 percent surge in cancellations, said Chief Executive Officer Alex Mashinsky. Business in New York from financial services companies fell by more than 25 percent in the past few months, he said.

Buying as Needed

Clients in recent weeks have narrowed the hours in which cars can be hired, Mashinsky said.

``Before things got worse, employees were allowed to take a car after 6 p.m.,'' he said. ``Now we see a trend to 8 p.m. or even 9 p.m.''

The falloff is especially noticeable at hedge funds and private equity firms, he said. ``The only business customers that are still strong are bankruptcy lawyers,'' Mashinsky said.

Businesses are buying as needed rather than planning a week or two in advance, said Bob Novatt, vice president of Jason Office Products on West 31st Street.

``Business is terrible,'' he said. ``They don't buy fine pens. They buy the staple items they need to run their business.''

Matan Feldman, CEO of the financial training company Wall Street Prep, says banks, hedge funds and private equity firms are signaling a slowdown in their 2009 spending. He expects ``more aggressive negotiations'' with clients, he said.

Republican presidents Hoover and Bush both used trickle down economics, and both have ended in economic turmoil. Unfortunately folks, the full impact of the current crisis hasn't been felt yet.

Here is an interesting link that could help explain the economic crisis:

http://news.yahoo.com/s/livescience/20081023/sc_livescience/outofthinairhowmoneyisreallymade

here it is again:

http://news.yahoo.com/s/

livescience/20081023/

sc_livescience/

outofthinairhowmoneyisreallymade

I told you so - in the face of the economic crisis?

I hope I heard wrong: a friend of mine asserted that no matter who wins the election, the other side will be able to say, "I told you so."

Reading the international headlines today, one can't help but think of what David Rockefeller once said, "We are on the verge of a global transformation. All we need is the right major crisis and the nations will accept the New World Order."

http://www.cnn.com/2008/WORLD/asiapcf/10/25/asia.europe/index.html

"Borrowed" from Ron Paul:

Why is it called the Federal Reserve? It isn't Federal (it's actually a private corporation) and it doesn't have any reserves?

excerpts from http://www.bloomberg.com/apps/news?pid=206...refer=worldwide

Nov. 10 (Bloomberg) -- The Federal Reserve is refusing to identify the recipients of almost $2 trillion of emergency loans from American taxpayers or the troubled assets the central bank is accepting as collateral.

Fed Chairman Ben S. Bernanke and Treasury Secretary Henry Paulson said in September they would comply with congressional demands for transparency in a $700 billion bailout of the banking system. Two months later, as the Fed lends far more than that in separate rescue programs that didn't require approval by Congress, Americans have no idea where their money is going or what securities the banks are pledging in return.

The collateral is not being adequately disclosed, and that's a big problem,'' said Dan Fuss, vice chairman of Boston- based Loomis Sayles & Co., where he co-manages $17 billion in bonds. ``In a liquid market, this wouldn't matter, but we're not. The market is very nervous and very thin.''

Bloomberg News has requested details of the Fed lending under the U.S. Freedom of Information Act and filed a federal lawsuit Nov. 7 seeking to force disclosure.

The Fed made the loans under terms of 11 programs, eight of them created in the past 15 months, in the midst of the biggest financial crisis since the Great Depression.

``It's your money; it's not the Fed's money,'' said billionaire Ted Forstmann, senior partner of Forstmann Little & Co. in New York. ``Of course there should be transparency.''

Federal Reserve spokeswoman Michelle Smith declined to comment on the loans or the Bloomberg lawsuit. Treasury spokeswoman Michele Davis didn't respond to a phone call and an e-mail seeking comment.

The following excerpt was cut and pasted from the "Rushed" transcript of the Lou Dobbs show that aired 11-10-08:

LOUISE SCHIAVONE, CNN CORRESPONDENT (voice-over): ... and Federal Reserve are working overtime to shore up the financial system but more and more, economists and strategists say what's missing are results and transparency starting with the massive loans now issued by the Federal Reserve. The Fed resisting calls to say who is getting them.

LEE SHEPPARD, CONTRIBUTING ED., TAX ANALYSTS: I don't think it should be OK with anybody right now. You know I -- Congress should want to know. The Fed is not, even though we want it to be independent, it's not you know it's not a power unto itself that makes its own laws. SCHIAVONE: The Federal Reserve tells CNN that about $1.5 trillion in loans have been issued by the Central Bank. It's an extraordinary amount of money, considering the fact that in the summer of 2007, outstanding Fed loans stood at 100 million. But out of concern for the reputations and soundness of the institutions involved, the Fed will not report who is getting the money now and what collateral they're using.

ROBERT MANNING, ROCHESTER INST. OF TECH.: Taxpayers are stretched thin and to tell taxpayers that it's not really any of their concern, where a trillion dollars may be headed, not to mention how much more there may be and will be after this, is really unconscionable.

SCHIAVONE: On a parallel track, the financial sector bailout which both the Treasury and analysts agree is not yielding immediate results.

DAVID SMICK, GLOBAL FINANCIAL STRATEGIST: The excess cash reserves of banks usually they lend to each other, it's usually somewhere between three and $7 billion, collectively for all the banks. I just looked up the number today, it's approaching 300 billion. They don't want to lend it.

SCHIAVONE: And people are losing their jobs.

PETER SEPP, NATIONAL TAXPAYERS UNION: All of these nightmare scenarios that were painted while this bailout was being debated are starting to come true.

By the way, the Fed Chairman and Treasury Sec. are appointed by the President.

CNN's Campbell Brown says Congress and the White House have "dropped the ball" overseeing the financial bailout. Her Commentary: Where's the oversight for $700B bailout?

It was less than two months ago that Congress passed the $700 billion bailout package. Do you remember how it went down?

Treasury Secretary Henry Paulson went to Capitol Hill, got down on his knees and begged House Speaker Nancy Pelosi, warning there would be financial Armageddon if he didn't get this cash.

He asked for a blank check. I criticized him for that at the time and applauded Congress for saying, "No way. There must be an oversight. You must account for the money you spend and answer to us every step of the way."

Well, what a joke. Because here we are today and more than a third of the $700 billion has been spent. Paulson tells us Wednesday, oh, by the way, he doesn't think the money is being spent the right way and he is now going to redirect the rest of it. Watch Campbell Brown's commentary

For all I know, Paulson is right. Maybe the original plan was a bad one and we do need to regroup. But where the heck is the oversight?

Full Article: http://www.cnn.com/2008/POLITICS/11/13/campbell.brown.paulson/index.html#cnnSTCText

A NEW GLOBAL CURRENCY

By Paul Proctor

March 26, 2009

NewsWithViews.com

It was reported recently that two of the world’s superpowers, Russia and China, have called for a new global currency. I believe they’re doing this because they know that the U.S. is printing huge amounts of dollars right now to pay on its own massive debts – debts that other countries, like China, have been financing for years by purchasing U.S. Treasury Bonds. They understand something that most Americans do not – that the more paper money you print, the less it’s worth – and right now, we’re printing it as fast as we can.

We owe China alone over a trillion dollars. And, that’s just one of many countries that we owe money to – countries that have also been buying our bonds.

You see, when you buy a bond, you’re loaning money and charging interest to the issuer of that bond to be paid upon maturity. If you buy a U. S. Treasury bond, you’re loaning the U.S. government money for them to spend as they see fit.

When you think of bonds, think of bondage.

Well, for years now, other countries have been buying our bonds so we could in turn buy all of their made-overseas stuff. They were essentially loaning their biggest customer the money we needed to buy from them.

That put us in financial bondage to them.

But, now that we’re not buying nearly as much from anyone anymore, resulting in millions of workers being laid off overseas as foreign factories close down, those countries are not buying as many of our Treasury bonds anymore either. In other words, they’re not loaning us near as much money as they once did.

So now, to get America’s bills paid, The Federal Reserve is purchasing those U.S. Treasury bonds other countries used to buy – and to do that, a lot more dollars have to be printed to buy them – and I mean a lot more, because, as most everyone knows by now, our debts are quite extraordinary and growing fast.

Well, who controls the printing of money?

You guessed it – the same folks who are loaning it to us by purchasing our bonds – a very secret and very private institution called The Federal Reserve. I’ll bet you thought they belonged to Uncle Sam, didn’t you? Nope, Uncle Sam belongs to them because, as the bible teaches, “the borrower is servant to the lender” and the lender here is The Federal Reserve.

For those who have a hard time understanding how all this affects the average person, let me put it as simply as I know how: It means that the price of everything you and I buy is going to start going up and up as The Federal Reserve has more and more money printed over the coming months and years until even the basic necessities of life here become unaffordable – or until the U.S. government steps in and starts initiating price controls, which frankly, is just more socialism.

When prices go up, it’s called “inflation.” And, if prices go up really high and really fast, it’s called “hyperinflation.” I prefer to call it what it really is: the deflation of the dollar. In other words, the goods and services we purchase day-to-day are not really increasing in value as much as the dollars we use to buy them with are decreasing in value.

They’re decreasing in value because The Federal Reserve has entirely too many of them printed up to loan out. Again, the more there is of something, including money, the less it’s worth.

This sleight-of-hand system, used by The Federal Reserve for decades, makes consumers blame producers, manufacturers, distributors and retailers for rising prices, when they should be blaming those who print all of that paper money for Congress to waste (I mean spend) – money that is not given to the U.S. government by the Federal Reserve, you understand, but is in fact loaned.

And guess who makes the payments on those loans from The Federal Reserve and pays all of the interest on those piles of paper money created out of nothing?

That’s right – you and I do – in the form of new and higher taxes.

So, every time a new “stimulus” package is announced, recognize it for what it really is: another huge loan to the American taxpayer to benefit somebody else with payments and interest you and I and our children and grandchildren after us (as taxpayers) will be responsible for paying back to that little private bank called The Federal Reserve.

Would you say the name is a little deceiving?

Over time, the American taxpayer gradually goes broke, even with money in the bank, and becomes the slave of a financial system built upon debt that he or she has absolutely no control over and can never repay.

You see, the loan can never be repaid in full because only the principal is created and loaned out by The Fed. You and I, the taxpayer, have to somehow come up with the interest. The Fed doesn’t print interest – only the principal – which means the taxpayer has to keep borrowing principal to repay interest that was never created to begin with.

Breathtaking, is it?

Now, Russia and China are calling for a new global currency because they know what’s coming: The dollar’s collapse into absolute worthlessness. Good grief, it’s barely worth 4 cents now compared to what it was when The Federal Reserve Act was passed back in 1913. So, frankly, it doesn’t have that far to fall; but fall it will, because The Federal Reserve is now mass-producing dollars to loan the U.S. government to pay its bills – which will all have to be paid back with interest (that was never created) to the very same people who made the money out of nothing but ink and paper and then loaned it to us.

Brilliant, huh?

Now, it’s becoming painfully clear to other countries, who have been footing our bills via U.S. Treasury bonds, that some other currency needs to be created ASAP to replace the dollar they’ve been forced to use (as the world’s reserve currency) before it collapses completely and leaves everyone around the world scrambling.

How this will actually play out over the next few years is anyone’s guess. Some believe regional currencies will emerge, like the controversial “Amero” which would purportedly serve the needs of Mexico, Canada and the U.S. in preparation for a world currency later, while others suggest the accelerating global financial crisis will compel the issuance of a world currency straightaway.

In the meantime, here are some questions for you to consider as all this unfolds in the coming days:

1. What’s going to happen to the dollars you have in the bank?

2. Will those dollars be exchangeable for the new currency, whatever it is?

3. If they are exchangeable, will they be worth what the new currency is worth or a lot less?

This is the fiscal future we face, my friends – a future of financial uncertainty.

http://www.newswithviews.com/PaulProctor/proctor177.htm

Post a Comment